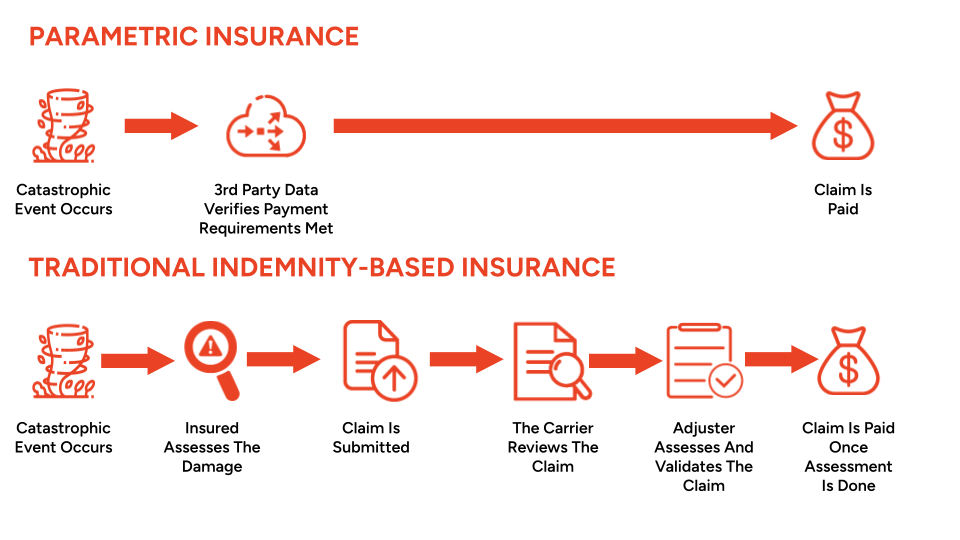

Picture the aftermath of a devastating natural disaster. Your client lost everything and now they have to deal with adjusters and a tedious claims process. Simultaneously, they are dealing with the urgency of immediate needs and out-of-pocket expenses like food and hotel. Imagine a world where you do not have to wait for a claim, the payout is sent within a few days, and there is no deductible. This is the reality with parametric insurance. What if you could provide your clients with protection to bridge the gap left by percentage deductibles, limitations, and exclusions in traditional policies (which only seem to keep growing), and eliminate claims paperwork?

Wesley Pergament, Sola

Wesley Pergament, Sola

Wesley Pergament, Sola

Wesley Pergament, Sola Wesley is CEO and Co-Founder of Sola Insurance based in Atlanta, GA. Wesley comes from a tech background and jumped into the insurance industry at a flood insurance startup where he was tasked with working on the data side with private and FEMA flood maps. Realizing this data was telling us exactly where the damage is, Wesley and the Sola team became obsessed with how data can be used to automatically trigger an insurance claim payout. Sola is starting with supplemental tornado coverage for homeowners and small businesses but plans to expand into every type of natural disaster to help people cover their deductible and immediate expenses. Sola has already been approved in 14 states as the first ever admitted personal lines parametric product, is fully reinsured through Lloyd’s of London and has partnered with dozens of agencies and aggregators.